What is a Loan Agreement PDF?

A loan agreement PDF is a digital document that outlines the terms of a loan between a borrower and a lender. This legal document serves as a tangible representation of the verbal or informal agreements made prior to the formal issuance of the loan. The primary purpose of a loan agreement PDF is to create a trackable trail for both the lender and borrower, detailing the specifics of the transaction.

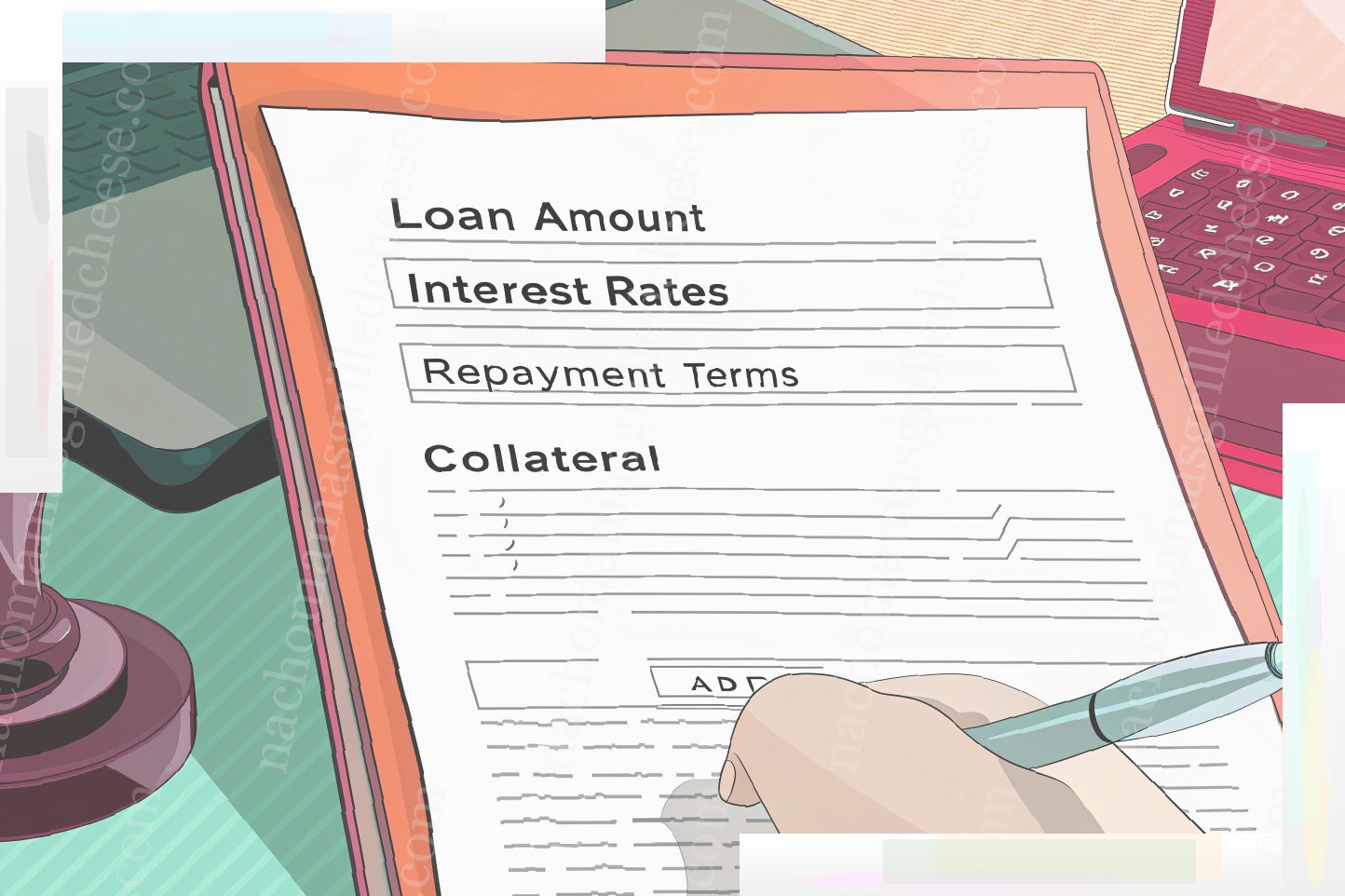

The components of a loan agreement PDF generally include the amount of the loan, interest rates, repayment terms, and collateral . In addition to these elements, the PDF may also contain sections on default, prepayment, transferability, and governing law. By including this level of detail, the PDF becomes not only an important financial document, but also a potential legal instrument.

Although verbal agreements can be made, having a written and signed loan agreement PDF can hold immense legal weight, making it an indispensable part of the process for serious borrowers and lenders.

Essentials of a Loan Agreement PDF

A loan agreement PDF will usually start with the basics, including the borrower’s and lender’s names, addresses, and contact information. This essential information enables easy communication throughout the loan term. A loan agreement must list the loan amount and outline the repayment terms and interest rate. It must also explain at what point the loan becomes immediately due in full, as well as what will happen if the borrower defaults. Additional considerations may include bankruptcy or death of either the borrower or lender.

The loan agreement PDF must also explain what happens in the event of a breach of contract or if one of the parties simply fails to live up to his or her end of the agreement. Will there be a penalty for late payment, and how much will it be? Will the lender seek recovery of his or her legal fees if the borrower defaults?

Other items that might appear in a loan agreement PDF are whether the lender or borrower has the ability to allow another person to take over the mortgage, if the borrower can refinance or sell the property to pay off the loan, and if the lender can also sell to someone else if the borrower defaults on making the payments.

The loan agreement PDF must usually include the notarized signatures of both the borrower and lender as evidence that both parties entered into the agreement willingly.

Downloading a Loan Agreement PDF Template

To download and use a loan agreement PDF template, first begin by searching for reliable legal websites that provide free templates for download. Websites such as LegalZoom, Rocket Lawyer, or specific government sites may have policies in place to offer these templates. Once you’ve found a site that provides a loan agreement PDF template for download, ensure that it is tailored to the specific loan type you need (Personal, Business, or Vehicle Transfer). It’s important to note that some sites may only offer templates for specific loan types, so it’s advisable to read through the descriptions before proceeding to download to make sure that it is the applicable template.

Once you’ve downloaded the template, open it in a PDF reader that allows for text editing. Fill out all of the appropriate fields, ensuring that all information such as the names, dates, type of currency used, loan amounts, terms of repayment, interest rates, governing law, collateral, governing provisions and signatures are inserted into the correct fields. As necessary, include any additional sections that may be required for your specific loan agreement, or delete any fields that may not be applicable to your situation. Ensure to save and rename your files accordingly for record-keeping purposes.

After filling out all of the necessary information, print out the final documents and have both parties sign them in the presence of a witness. At this point, the loan agreement is ready to be executed, and you have fulfilled the requirements for a legally binding loan agreement. Now, all that is left is to hand a copy to the borrower and keep one for your own records.

Legal Aspects of Loan Agreements

Many people do not consider the legal implications of signing a loan agreement as a PDF document. However, it is important to be aware of these issues prior to commencement of transaction and especially before the loan agreement is signed. Understanding your legal position can help avoid problems and disputes in the future. This section provides an overview of some of the key legal considerations.

Legal advice

The loan agreement represents a significant financial commitment. Therefore, it is prudent to seek legal advice prior to agreeing to the loan agreement and before the agreement is signed, particularly if the terms are complex or there may be a degree of uncertainty about the arrangement. You should also ensure that the other persons involved in the arrangement also seek independent legal advice. Failure to do so may adversely affect your ability to claim your rights under the loan agreement or under separate legislation.

Legal risks

By signing a loan agreement, the person executing the agreement is agreeing to be legally bound by those terms, whether or not the person intends to be bound. The person executing the agreement should carefully read and understand all the terms of the loan agreement prior to signing it. Although you will generally be entitled to rely on the terms of the loan agreement, it is also important that you are aware that in some cases an agreement may be unenforceable or void. For example, in some circumstances a loan agreement may be unenforceable if the lender is registered with the Personal Property Securities Register (PPSR) and the loan agreement is not noted on the PPSR.

The loan agreement may also be challenged, or declared unenforceable or void, if it envisages unconscionable or prohibited conduct in the relationship between the parties. For example, a loan agreement may be unenforceable or void if the lender took unfair advantage of the borrower.

It is crucial that the loan agreement be fully understood and that the lender takes all necessary steps to protect its interests. If you are concerned about the enforceability of the loan agreement, it is advisable to seek legal advice.

Compliance with law

Regardless of how the loan agreement is signed, it must comply with all relevant laws applicable to loan transactions. Failure to comply with these requirements may result in the loan agreement being unenforceable and/or void. For example, the lender may be required to be registered with the Australian Credit License scheme and comply with legislative disclosure and reporting requirements. Additionally, there is a range of consumer protection legislation in Australia and New Zealand that is designed to protect consumers in relation to financial transactions. Disclosing the terms and conditions of a loan agreement can help to mitigate these risks.

Common Pitfalls in Loan Agreement PDFs

The most common mistakes you are likely to encounter from the loan agreement pdf

A loan agreement pdf will usually have a section of standard definitions. So once you finish reading the contract text itself, you may start flipping back and forth between the two. If this is making it difficult to understand the meaning of terms and parties used in the agreement – instead of going back, I suggest you find the relevant definitions first.

You may come across conditions that make it hard to grasp or apply the terms. For example, you will see a ‘guarantor’ and ‘security agent’ being mentioned. It will be a good idea to have a brief research about what these roles mean and how they are performed. This is because the parties’ obligations under the loan will usually depend on these counterparts.

Some of the errors that some contracts may have when it comes to the loan agreement pdf are:

One common mistake in a contract stipulates that your credit will be affected in case you are not able to cover your loan. However, this clause is not legally binding. Your loan certainly has an impact on your credit rating, but it’s important that you go over state laws and regulations to see your rights as a borrower before signing something that’s more of a suggestion than a binding requirement .

Another common loan agreement pdf mistake is the lender claiming they are not legally obligated to approve your loan. While this could be true in the sense that it is possible for the lender to cancel the loan agreement at any time, it’s also clear that they have to meet the requirements they laid out before they offered you the loan in the first place.

If the loan agreement stipulates that your signature and date must be confirmed by a public notary – which is common for larger loans, like mortgages – ensure the person signing as a witness is an authorized notary. Some lenders may have their own in-house public notaries, but always make sure.

One of the most common loan agreement mistakes is the absence of precise amounts. This might be the amount you’re borrowing, the interest rate, the timelines and, in some cases, even the term of the contract. Make sure you know what you’re signing up for.

Any loan agreement pdf that you sign shouldn’t be unfair. Your rights as a borrower shouldn’t be put the mercy of the lender. This is especially crucial with unsecured loans.

Unless otherwise stated, once you have signed the loan agreement pdf, you should take it as granted unless you actually reach an agreement between you and the lender. Most lenders will make sure that not all terms require renegotiation. This is counterproductive as well.

The Significance of a Signed Loan Agreement PDF

The signed version of the loan agreement is extremely important. Defintely keep it in a safe place. You will want to use it as evidence in case of issues. Many times I have found that parties try and make claims about what the loan documents say that were inconsistent. If you have the signed version in PDF format you can use it at court or communication with lenders to show that the documents meant something different from what the lenders said they meant.

It is also important to keep the loan agreement pdf because sometimes bank and credit unions will change their forms. They will say that the original loan agreement expired or have different forms for business and commercial loans. This is nonsense. You are protected by the statute of limitations (a period of time during which legal action can be taken on a loan agreement). In Washington, that is a six year statute of limitations. Sometimes the bank or credit union will say, "I can’t help you, you must have signed a different loan agreement." This can be rebutted if you have the signed loan agreement in PDF format. Simply email the lender or creditor the loan agreement signed agreement in PDF format, and they will have to honour your position.

When going through all of your old loan documents I strongly suggest choosing bank formats or at least having all of your loan documents in the same format. Some banks charge and some do not but dealing with large amounts of documents can be cumbersome. Be sure to write down the dates on which specific loan agreements were signed if you are completing forms.

Technological Innovations in Managing Loan Agreement PDFs

The advent of the Personal Computer and later the Internet has transformed how many businesses conduct their activities. The legal world has not been untouched, particularly as businesses seek to transfer the burden of keeping up with ever-evolving technology to their lawyers.

Lawyers have always focused on value and cost, and while we still need to physically meet with clients, email is often the preferred means of communication. Now, solutions exist to make contract management and execution even more efficient than ever before. Sophisticated legal software platforms facilitate the creation and management of loan agreements in a fraction of the time that traditional methods would require. Combining these platforms with electronic signature technology, such as DocuSign or an equivalent, has made the management and execution of loan agreements much more efficient than ever before. Especially in cases where a loan document is to be reviewed and executed by a number of parties, both within and without the same organization, this can translate into days if not weeks .

Some of the advantages of electronic signatures include:

Dawn Of The Electronic Signature

The US Electronic Signatures in Global and National Commerce Act ("E-Sign Act") 2000, along with the Uniform Electronic Transactions Act ("UETA") 2000, (which addresses the legal situations in which signatures may be required) support electronic signatures and access to loan documents. The E-sign Act was passed in 2000 and provides a uniform legal framework under which individuals throughout the United States may enter into contracts and forms of agreements electronically. The underlying principle of the E-sign Act is that an electronic signature should be treated just the same as a handwritten signature and that any transaction legally required to be in writing may be conducted electronically. As of today, about 47 states have adopted a version of the Uniform Electronic Transactions Act into law, and at least 20 states have adopted the UETA into law. The UETA also supports the use of electronic signatures and allows the use of an electronic replica of a loan document for purposes of signature collection. However, even if one jurisdiction does not support the UETA, the E-sign Act, which is federal law, preempts all inconsistent state laws. Therefore, the use of an electronic loan document and electronic signature is legal in almost all cases.

Leave a Reply